Running a dental office means you’re not just delivering care—you’re also running a high-trust, high-compliance business where the payment experience can either strengthen patient relationships or quietly weaken them. The “best credit card processors for dentists” aren’t simply the ones with the lowest posted rate.

The best-fit option is the one that matches how your practice collects money (chairside, front desk, online, recurring plans), how your team uses practice management software, how often insurance creates partial balances, and how strict you want to be about security, disputes, and patient communication.

Modern dental payments have also changed. Patients expect tap-to-pay, text-to-pay, and online pre-pay. Practices want fewer manual steps, fewer statement errors, faster deposits, and clean reporting that makes end-of-day reconciliation painless.

Payment providers are responding with integrated payments inside dental software, payment links, digital wallets, automatic receipts, and better chargeback tooling. Stripe’s own overview of dental payment processing highlights that the “payment system” is broader than a terminal—it spans scheduling to final collection after insurance adjudication.

This guide is written for practice owners and office managers who want a practical, updated way to choose credit card processors for dentists without getting trapped in confusing pricing, long contracts, or the wrong hardware.

You’ll see how to evaluate processors, what features matter specifically for dental, how to compare pricing models, how to stay compliant, and what changes may reshape costs in the next couple of years—including PCI DSS v4.x deadlines and evolving surcharge rules.

What “Best Credit Card Processors for Dentists” Actually Means in a Dental Office

In dentistry, payments aren’t a single swipe at checkout. The workflow is layered: appointment deposits, estimates, copays, split tender (HSA/FSA + card), financing plans, and post-insurance patient portions that arrive weeks later.

That means the best credit card processors for dentists must handle partial payments cleanly and support follow-up collection without creating staff chaos.

A processor can look “cheap” on paper and still cost you more through hidden line items, poor patient support, slow funding, or clunky reconciliation. Dental practices also tend to have higher average tickets than many retail businesses, which changes what pricing model wins.

If your average card ticket is $250–$1,000 and your monthly volume is consistent, you may benefit from interchange-plus or subscription models that reduce the processor’s margin on percentage fees. If your practice volume is smaller or unpredictable, flat-rate simplicity can be worth it.

Another dental-specific factor is patient experience. A clean payment flow reduces uncomfortable conversations. Think of features like saved cards for treatment plans (with proper consent), secure payment links, automatic email/text receipts, and the ability to take payments by phone without writing card numbers on sticky notes.

Some processors also align better with dental software and reduce duplicate data entry—one of the biggest hidden costs in a front office.

So, when we say “best credit card processors for dentists,” we’re really talking about processors that deliver five outcomes: predictable costs, smooth patient payments, strong security, reliable deposits, and clean reporting that matches how dental billing actually works.

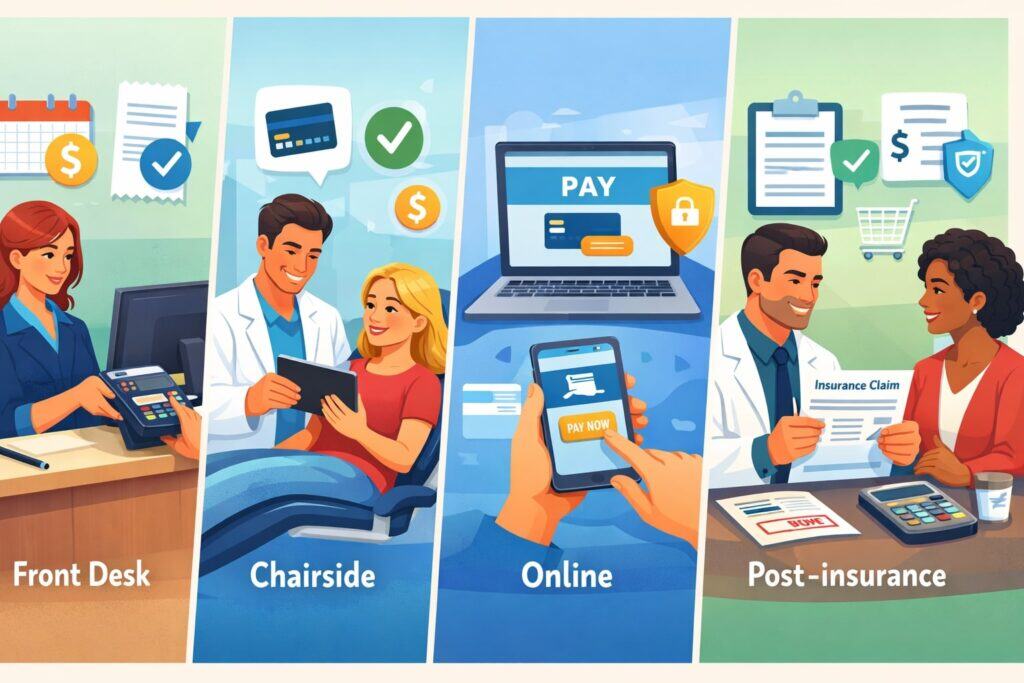

Dental Payment Workflows That Your Processor Must Support (Front Desk, Chairside, Online, and Post-Insurance)

Most dental offices collect payments in at least four ways:

- Front desk payments: The classic checkout swipe/tap/dip, often with printed receipts and a need for quick refunds or adjustments.

- Chairside payments: Increasingly common for practices that want to finalize same-day treatment payments without sending the patient back to the desk. This requires mobile terminals or tablet-based checkout.

- Online payments: Patients want to pay from a link—especially for deposits, missed appointment fees, or remaining balances after insurance. Many practices also want online “pay my bill” pages.

- Post-insurance follow-ups: The hardest part of dental collections. When insurance pays less than expected or denies a code, the remaining patient portion must be collected without friction. That’s where secure stored credentials (tokenization), recurring billing tools, and automated reminders become valuable.

A processor that’s great for retail can struggle with dental reality if it doesn’t support invoicing, stored payment methods, or easy “card on file” with clear patient authorization. Stripe’s dental payment explainer frames dental payment processing as everything from scheduling to the last cent collected after insurance settles, which matches what practices experience daily.

The best credit card processors for dentists also offer flexible acceptance: contactless (NFC), EMV chip, magstripe fallback (limited), keyed entry for phone payments, and digital wallets. And they must support how dental teams work: multiple users, role-based permissions, audit logs, and exports that map to your accounting approach.

If your processor can’t handle these workflows gracefully, you’ll feel it in staff time, patient complaints, and higher A/R—no matter how attractive the rate looks.

The Most Important Features to Look for in Credit Card Processors for Dentists

When choosing credit card processors for dentists, focus on features that reduce errors, reduce labor, and protect the practice.

1) Integration with dental practice management software

Integrated payments can reduce duplicate entry and improve reporting consistency. Many dental platforms and industry voices are emphasizing integration as a major direction for practices because it streamlines billing and reduces staff stress.

2) Tokenization and secure “card on file”

This is essential for treatment plans, recurring payments, and post-insurance balances. You want tokenized storage (the processor stores a token, not raw card data), plus a workflow for capturing written or digital authorization.

3) Payment links, text-to-pay, and online invoices

Patients increasingly expect remote payment options, and practices benefit because it shortens time-to-cash.

4) Fast funding and predictable deposits

Same-day or next-day funding is valuable, but consistency matters more than promises. Understand cutoffs and weekends.

5) Dispute and chargeback tooling

Dentistry has fewer chargebacks than some industries, but when they happen, you need easy retrieval of receipts, signed treatment plans, and patient communications.

6) Transparent pricing and a clean statement

The best credit card processors for dentists make fees understandable: interchange, assessments, and the processor markup. If your statement is unreadable, it’s hard to control the cost.

7) Hardware options that fit your office

Countertop terminals, mobile devices for chairside, and a backup method if the internet goes out.

8) Support that understands healthcare-style billing

Generalist support can struggle with dental edge cases like partial insurance payments and multi-step collections.

In short: prioritize operational fit over marketing claims. The best processors lower administrative friction, not just basis points.

Pricing Models Explained for Dental Practices (Flat Rate vs Interchange-Plus vs Membership)

Pricing is where many practices get burned, so it’s worth understanding the models before you compare “best credit card processors for dentists.”

Flat-rate pricing

Flat-rate providers advertise a simple fee for card-present and online transactions. This is easy to budget and easy for smaller practices. The downside is you often pay more than necessary on debit and lower-cost cards because the provider averages costs across all card types.

Interchange-plus pricing

Interchange is the underlying cost set by card networks and issuing banks; the processor adds a fixed markup (“plus”). Many transparent providers emphasize interchange-plus because it makes the processor’s margin visible. Helcim, for example, publicly positions its pricing as interchange-plus.

This model is frequently a strong fit for dental practices with consistent volume and higher average tickets, because you’re not overpaying as much on cheaper cards.

Membership/subscription pricing

Membership models often charge a monthly fee and then pass interchange through with reduced or zero percentage markup (still usually with a per-transaction cents fee). Stax markets subscription-based plans, and multiple reviews note this model can benefit businesses processing at least several thousand per month.

For a dental practice with steady volume, membership pricing can be a real win—but only if the monthly fee doesn’t exceed the savings.

Dental-specific pricing traps to watch

- “Non-qualified” tiers (avoid tiered pricing when possible)

- Extra gateway fees for online pay

- PCI program fees that don’t match your true compliance scope

- Long-term leases on terminals

- “Free” equipment that locks you into high rates

The best credit card processors for dentists will explain pricing in plain language and provide sample statements—not just a teaser rate.

The Shortlist: Best Credit Card Processors for Dentists (By Practice Type)

There isn’t one universal winner. Instead, the best credit card processors for dentists depend on your practice model. Below is a practical shortlist by “best fit” category, using widely used payment platforms and pricing approaches that are current and well-documented.

Best for modern online + software-driven practices: Stripe

Stripe is strong for practices that want online payment links, portals, developer-friendly integrations, and a broad payments platform. Stripe publishes its standard pricing and is commonly used for online payments and embedded payment experiences.

- Why it can be “best” for dentists: If you offer online deposits, payment plans, or you’re building a branded billing flow, Stripe’s tooling is flexible.

- Watch-outs: You’ll want a clear plan for in-person terminals, refunds, and reconciliation with dental software.

Best for all-in-one simplicity at the front desk: Square

Square is often chosen when a practice wants quick setup, straightforward pricing visibility, and easy in-person acceptance without negotiating a custom merchant account. Square provides a public fee breakdown page for its payments.

- Why it can be “best” for dentists: Simple staff training, easy hardware options, and strong day-to-day usability.

- Watch-outs: Flat-rate simplicity can cost more at higher volume, and some practices want more control over statements and fees.

Best for transparent interchange-plus with built-in tools: Helcim

Helcim emphasizes interchange-plus pricing publicly and targets businesses that want transparency without “mystery fees.”

- Why it can be “best” for dentists: Predictable markup structure, useful payment tools, and a pricing posture that fits practices wanting clarity.

- Watch-outs: Confirm how it integrates with your specific dental software and how quickly funds settle for your bank.

Best for higher-volume practices that want membership pricing: Stax

Stax promotes transparent pricing plans, and third-party reviews frequently describe Stax as a fit for businesses with meaningful monthly card volume.

- Why it can be “best” for dentists: If you process significant volume, subscription pricing can reduce percentage markups and improve predictability.

- Watch-outs: Membership fees must be justified by savings; confirm total cost with your actual volume mix.

Best for practices committed to integrated dental payments

If you’re using a dental practice management system that offers integrated processing, that “embedded” option can be the best credit card processor for dentists from a workflow standpoint—because it reduces clicks, reduces posting errors, and improves end-of-day close. Industry content increasingly points to integrated payments as a forward direction for dental practices.

Watch-outs: Integrated options sometimes limit your ability to negotiate rates. Ask for a full fee schedule and a contract review.

This shortlist gives you a real-world map: pick the category that matches your practice operations, then evaluate two or three providers in that category.

How to Evaluate a Processor Like a CFO (Without Getting Lost in Sales Talk)

To identify the best credit card processors for dentists, treat the decision like a financial system upgrade, not a commodity purchase.

Start with your numbers

Pull three months of processing statements and calculate:

- total monthly volume

- average ticket size

- percent card-present vs online vs keyed

- chargebacks/refunds count

- funding speed and deposit frequency

Even small differences in fee structure can matter a lot with higher average tickets.

Demand clarity on the “effective rate”

Sales reps often quote a teaser rate that excludes fixed fees, monthly fees, PCI fees, gateway charges, and “non-qualified” surcharges (in tiered plans). Ask for an estimate of your effective rate using real statements.

Check operational friction

A processor that saves 0.10% but adds 30 minutes of front-office time per day is not a win. Test: refunds, partial payments, post-insurance billing, and receipt retrieval.

Validate support quality

Dental offices need quick answers. Ask: What are support hours? Is there phone support? Is there a dedicated account manager? How do you escalate a funding hold?

Contract and cancellation reality

If there is a term contract, ask for: length, early termination fee, PCI program fees, and equipment terms. Avoid terminal leases where possible.

Integration proof

If someone claims “we integrate with your dental software,” ask them to demonstrate the actual workflow, not a generic API explanation.

The best credit card processors for dentists are the ones that can prove total cost and workflow benefits with your real numbers, not generic promises.

Compliance and Security: PCI DSS v4.x, Patient Data, and Dental Reality

Dentistry is a high-trust environment, and payment security failures damage more than finances—they damage reputation.

PCI DSS v4.x matters right now

PCI DSS v4.0 introduced new requirements that became mandatory after a transition period, with key future-dated requirements moving into enforcement around March 31, 2025 (depending on the exact requirement and version). Multiple PCI-focused summaries highlight that March 31, 2025 is a major milestone when new v4.0 requirements become mandatory.

For dental practices, this usually translates into: stronger password and MFA expectations, better logging/monitoring, and more disciplined vulnerability management—especially if you run any payment pages or systems that touch cardholder data.

HIPAA and card payments—what to know

Card payment data itself is governed by PCI rules, but patient information is regulated separately. The key operational point: never mix card data with patient notes and never store card numbers in your practice management system, email, or spreadsheets. Use tokenization and compliant payment tools.

Practical controls that protect dental practices

- Use EMV + contactless terminals (reduces counterfeit fraud risk)

- Lock down user permissions and turn off shared logins

- Train staff on phone payments (no writing card data)

- Use secure payment links instead of collecting card details via email

- Segment your network if you have multiple devices

- Keep systems patched and supported

Even if you outsource most payment risk to your processor, your office procedures still matter. The best credit card processors for dentists help with compliance tooling, but you must pair that with good internal habits.

Surcharging, Convenience Fees, and Cash Discounts (What’s Changing and What Dentists Should Watch)

Rising processing costs lead many practices to consider passing fees to patients. This area is sensitive because dentistry relies heavily on trust and long-term relationships.

Surcharging is not “set and forget”

Dental industry guidance and state-level discussions emphasize that surcharging can be legal in many places, but it comes with card-network rules, disclosure requirements, and state law nuances. Dental-focused guidance warns practices to understand both the legal and reputational risks before implementing surcharges.

Why this is an “updated” issue

Recent updates highlight that rules and enforcement attention continue to evolve, and dental practices need to get it right in 2025 and beyond. If you surcharge incorrectly, you risk complaints, refunds, and potential network issues.

Better alternatives in many dental settings

- Cash discount programs (structured carefully)

- Debit steering where allowed and supported

- ACH for larger balances (if your processor supports it)

- Offer financing for big cases instead of trying to surcharge high-ticket card payments

- Improve collections with text-to-pay and card-on-file authorization so balances get paid faster (reducing aging and follow-up cost)

The patient communication angle

If you do anything fee-related, disclose it early: on the website, in estimates, and at scheduling—not at the moment of payment. Dental manager guidance emphasizes that surprise fees can erode trust.

For many offices, the best credit card processors for dentists are the ones that help you reduce fees through smarter pricing and debit/ACH options rather than forcing a surcharge strategy that creates patient friction.

Hardware for Dental Offices: Terminals, Mobile Devices, and the “Front Desk + Chairside” Setup

Hardware choice can quietly make or break your payment workflow.

Countertop terminals for the front desk

A reliable EMV + contactless terminal with a fast receipt workflow is still the core for many offices. Look for:

- tap, chip, swipe fallback

- wired ethernet option (more stable than Wi-Fi)

- fast void/refund process

- multi-user shift controls

- clear receipt reprint

Mobile devices for chairside collections

If you collect in operating rooms, mobile card readers or handheld terminals reduce the “I’ll pay at the desk later” drop-off. It also fits practices that want a more hospitality-like experience.

Dual setup best practice

Many practices benefit from a dual approach: countertop at front + mobile backup device. If the internet goes down, having LTE backup (or a manual “card on file” token workflow) prevents operational disruption.

Don’t lease equipment blindly

Leasing is often the most expensive way to acquire hardware. If a processor pushes a long lease, ask for a purchase option or bring-your-own-device support.

Match hardware to the software plan

If you’re choosing an integrated platform, the “best” terminal is the one supported natively by your payment integration, because it reduces troubleshooting. Stripe and Square both support ecosystems that can include in-person acceptance paired with online payment tools, but the best fit depends on how you run your office.

When evaluating the best credit card processors for dentists, make hardware a first-class decision, not an afterthought.

Online Payments, Text-to-Pay, and Patient Portals (Where Dental Collections Are Heading)

Patients increasingly prefer remote payment options, and dental practices benefit because remote payments reduce billing friction and speed up cash flow.

Online “pay now” options reduce A/R

The biggest win is often post-insurance balances. Instead of sending multiple statements, your team can send a secure link with a clear balance due and payment confirmation.

Payment links and invoices

These are especially useful for:

- appointment deposits

- missed appointment fees

- whitening packages

- aligner plan monthly payments

- remaining balances after insurance

Patient portals and integrated platforms

A portal that shows balances and payment history can reduce calls and confusion. Stripe’s dental overview highlights that payment processing covers the entire timeline from scheduling through final collection, which aligns with the portal approach.

Future trend: more automation, less phone tag

Expect more practices to adopt automated reminders, scheduled payment plans, and “file-on-token” recurring collections—because staffing remains tight and manual follow-up is expensive. Industry discussion around integrated payments supports this direction as a way to reduce staff stress and improve the patient experience.

If you want your article’s main promise—finding the best credit card processors for dentists—this is one of the clearest indicators: choose a processor that makes remote payment effortless and secure, because that’s where dental billing is moving fastest.

Cost-Control Strategies That Don’t Hurt Patient Trust

Reducing processing cost is important, but dentistry is not a commodity retail environment. You can’t optimize purely for pennies if it creates awkward moments with patients.

Negotiate based on real volume

If you use interchange-plus or membership pricing, your negotiation leverage increases with consistent volume and low risk. Present clean statements and ask for a simplified fee schedule.

Reduce keyed transactions

Keyed transactions cost more and carry more fraud risk. Move phone collections to secure payment links or a compliant virtual terminal workflow.

Use ACH for big balances (when appropriate)

For large cases, ACH can be cheaper and predictable. The “best credit card processors for dentists” often support multiple rails (card + ACH) so you can choose the right method.

Improve authorization and documentation

Good documentation reduces disputes and improves collections: signed treatment plans, clear estimates, and consistent receipts.

Reconcile daily

Daily reconciliation prevents the “mystery balance” scenario and catches errors early.

Be careful with fee pass-through

As discussed, surcharging and similar tactics can be legally and operationally complex and can damage patient goodwill if done poorly. Dental-specific guidance encourages careful consideration and communication.

A processor that helps you implement these strategies cleanly is often truly the best credit card processor for dentists—even if its headline rate isn’t the lowest.

Future Predictions: What Will Change for Dental Payment Processing in 2026–2028

The next few years will likely reshape what “best credit card processors for dentists” means.

1) More integrated payments inside dental software

The momentum is toward “payments embedded into workflow,” not standalone terminals. Integrated payments reduce staff time and improve reporting consistency.

2) PCI compliance expectations will keep rising

As PCI DSS v4.x requirements become fully standard, even small practices will face higher expectations for authentication, monitoring, and secure procedures. The March 2025 milestone for v4.0 requirements is a clear signal: security obligations are trending upward, not downward.

3) Pressure on card fees may continue

There have been ongoing disputes and negotiations in the market about interchange and acceptance rules. Reuters reported in late 2025 about Visa and Mastercard being near a settlement with merchants that could reduce certain fees and alter some acceptance dynamics (subject to approval and details).

For dental practices, this could mean modest changes—not a sudden fee collapse—but it’s worth watching because it may affect pricing and the value of steering tools.

4) More “pay by link,” more remote-first collection

Patients will continue to expect digital-first experiences. Practices that offer convenient remote payment will likely see faster collections and fewer billing calls.

5) Data and automation will become a bigger differentiator

Processors and platforms are building smarter dashboards and operational tools. Over time, the “best” providers will be the ones that reduce administrative work, not just process payments.

The takeaway: choose a processor that’s aligned with integration, security modernization, and digital collection—because those trends are not reversing.

FAQs

Q.1: What is the best pricing model for a dental practice: flat rate or interchange-plus?

Answer: For many practices, interchange-plus tends to be the best long-term fit once volume becomes steady and meaningful, because it separates the underlying interchange cost from the processor’s markup.

This transparency makes it easier to compare offers and reduces the chance you’re paying an inflated blended rate. Providers that promote interchange-plus publicly often position it as a way to avoid hidden tiers.

That said, flat-rate pricing can be “best” early on because it removes complexity and makes costs predictable, especially when a practice has lower volume, fewer staff, or limited time to analyze statements. Square, for example, emphasizes clear fee breakdowns to help businesses understand what they pay.

The most practical way to decide is to compare both models using your own last 90 days of statements. The best credit card processors for dentists will run a side-by-side cost simulation using your real transaction mix (debit vs rewards, card-present vs keyed, etc.). If a provider won’t do that—or refuses to provide a clean fee schedule—that’s a red flag regardless of model.

Q.2: Do dentists need “HIPAA-compliant credit card processing”?

Answer: Dentists need strong privacy and security practices, but the phrase “HIPAA-compliant credit card processing” can be misleading if used as pure marketing. In practice, your responsibilities are split into two areas: payment security (PCI DSS) and patient information privacy (HIPAA-related obligations).

The operational goal is to keep these worlds cleanly separated—don’t store card numbers in patient records, don’t email card details, and don’t write card data down.

Where processors help is by offering tokenization, secure payment links, compliant virtual terminals, and workflows that minimize your exposure to card data.

At the same time, PCI standards are evolving, and the shift toward PCI DSS v4.x requirements becoming mandatory (with major enforcement milestones around March 2025) underscores that security expectations are rising.

So, the best credit card processors for dentists are typically the ones that reduce your compliance burden with modern tools and clear documentation—while you maintain sound internal procedures for staff training and device security.

Q.3: Can dental practices add a surcharge to credit card payments?

Answer: In many states, surcharging can be legal, but it is complicated and highly sensitive in a dental environment. Card networks have rules, and states may have their own restrictions or disclosure requirements.

Dental-focused guidance stresses that practices should understand legal and contractual conditions and communicate clearly to avoid surprising patients.

Even when it’s permitted, many practices decide it’s not worth the reputational risk. Dentistry relies on trust, and a fee at checkout can feel like a penalty—especially when patients are already dealing with insurance confusion.

If you go this route, the best approach is transparency: disclose before the appointment, on estimates, and with signage, and ensure your processor supports compliant handling.

For many offices, a better strategy is lowering total processing cost through pricing negotiation, shifting larger balances to ACH, reducing keyed transactions, and improving collections with text-to-pay. Those tactics often produce savings without turning the payment moment into a conflict.

Q.4: Should a dental practice use an integrated processor inside its dental software?

Answer: Often, yes—if the integration is well-built and the pricing is fair. The main advantage is workflow: fewer manual steps, fewer posting mistakes, smoother end-of-day reporting, and faster staff onboarding.

Industry commentary increasingly describes integrated payments as a future direction for dental operations because it strengthens patient trust and reduces administrative load.

The tradeoff is negotiating power. Some integrated solutions limit your ability to shop rates, add certain payment methods, or use preferred hardware. That doesn’t mean they’re bad—many times they’re the best credit card processors for dentists from an operational standpoint—but you must review the complete fee schedule and contract terms carefully.

A smart approach is to ask the dental software vendor and the processor to walk through real scenarios: partial insurance payments, refunds, recurring payments, and reporting exports. If those scenarios are smooth, integration can be a major advantage.

Q.5: What’s the simplest way to compare two processors for a dental office?

The simplest method is to compare using three items: (1) your last 2–3 statements, (2) your workflow needs, and (3) a written quote with a full fee schedule.

Start by calculating your effective rate (total fees ÷ total card volume). Then break down your transaction mix: card-present vs online vs keyed, average ticket, and monthly volume. Next, test workflow fit: can you take deposits online, send text-to-pay links, store a tokenized card with authorization, and collect post-insurance balances without awkward manual steps?

Finally, make the provider put it in writing. Stripe publishes standard pricing publicly, which can be useful as a baseline, and Square provides a fee breakdown page that helps compare simplicity vs optimization.

If a provider won’t provide a clean quote or tries to hide behind vague promises, they’re unlikely to be one of the best credit card processors for dentists—no matter what they claim.

Conclusion

Choosing the best credit card processors for dentists is less about chasing the lowest advertised rate and more about matching your payment system to how dental billing actually works.

The right processor supports front desk and chairside payments, online deposits, post-insurance patient balances, payment links, and secure stored payment methods—without turning your office into a finance department.

Start with your workflow, then evaluate pricing models with real statements. Flat-rate simplicity can be fine for smaller practices or teams that want speed and predictability, while interchange-plus or subscription pricing can reward consistent volume and higher average tickets.

Public pricing references from platforms like Stripe and fee breakdown transparency from Square can help you anchor your comparisons.

Don’t ignore compliance. PCI DSS v4.x deadlines and evolving requirements make security and process discipline more important than ever, and the market is moving toward integrated payments and digital-first collections that reduce staff time and improve patient experience.